The short-term outlook for ag retailers is positive given a backdrop of strong farmer income and steady demand for crop inputs. As harvest concludes later this fall, farm supply cooperatives (barring any weather shocks) should experience an active and profitable fall agronomy season. Further, with corn and soybean futures prices above the cost of crop production, the good times could last throughout the next 12 months.

The traditional approach for farm supply cooperatives is to save above-average profits when times are good (like now through the next 12 months) and then manage costs rigorously during the inevitable downturn, which we expect will begin in 2023.

Unfortunately, this approach exposes cooperatives to revenue volatility and declining earnings during down cycles, often lasting five or more years. We see an alternative path forward for ag retailers: expand their delivery of precision agronomy tools, services and processes, and earn fee income for doing so. Putting technology and information to work to help farmers manage their inputs and production is where farm supply co-ops excel. The current upturn in the crop cycle provides a timely opportunity to make the necessary investments in technology-experienced staff who can develop revenue sharing partnerships with partners across the value chain.

Farm supply cooperatives are enjoying success given current favorable U.S. farm economics

Ag retailers have enjoyed three consecutive profitable agronomy seasons and generally appear well positioned for fall 2021 amidst high grain prices and favorable farm economics (the partial risks to this outlook include weather volatility, expected shortages of certain crop production chemicals, and high fertilizer prices that may cause growers to ration purchases).

Notwithstanding the known risks, three factors support a continued favorable environment for input spending:

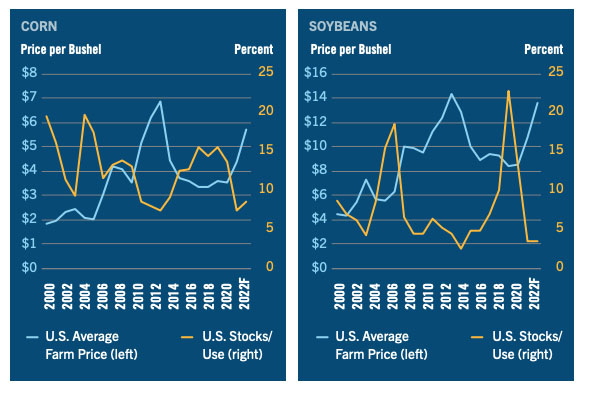

- Cash corn, soybean, and wheat prices. Grain prices are currently well above the 2014-19 averages of $3.77 for corn, $9.56 for soybeans and $4.98 for wheat.

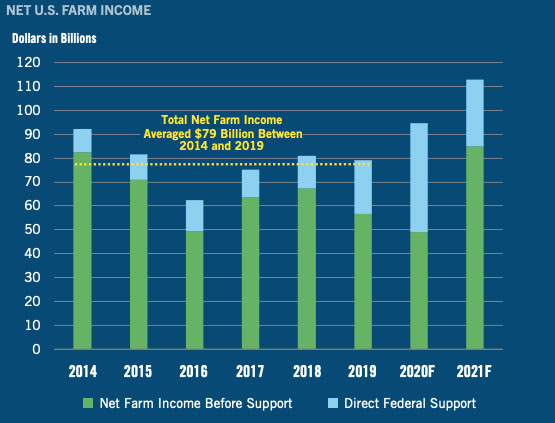

- Strong net income. Industry sources estimate that U.S. net farm income will reach $111 billion for 2021 and $104 billion for 2022, versus average net farm income of $79 billion between 2014 and 2019 (i.e., the period prior to the recent “grain run”).

- Favorable cash flows. Cash crop receipts, a cash flow proxy, are forecasted to reach $216 billion for 2021 and $221 billion for 2022, versus an average of $196 billion between 2014 and 2019.

Tight stocks-to-use in 2022 should support higher corn and acres and therefore, continued above-average crop prices and input demand

U.S. corn and soybean stocks remain very tight (at or near levels last seen during 2012- 14), a situation that we see continuing for the near future. What led the industry here was a combination of 1) strong domestic and export demand (especially from China) for food, feed and fuel, coupled with 2) lower production in Brazil, Argentina, and China in 2020 and 2021 resulting mainly from adverse weather (drought and freezes). What will keep the industry here is continued strong exports (see next page) and growing demand for oilseeds. Considering all factors, we see the demand imbalance in grain stocks and usage persisting until at least 2023.

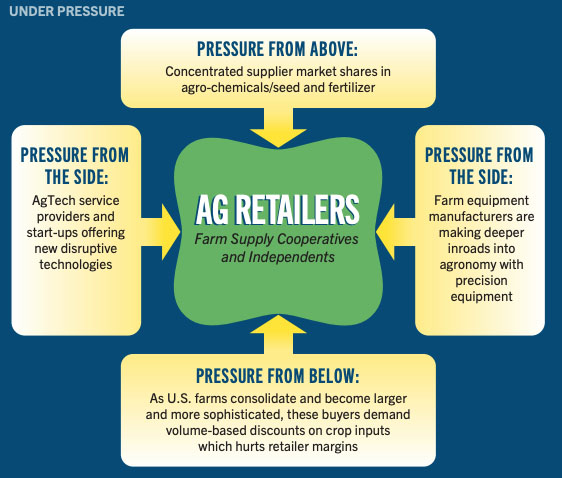

Looking out several years, ag retailers will face increasing pressures from all sides

Ag retailers are facing risks that will only increase over time including the consolidation and growing market power of agro-chemical and seed suppliers and the maturation of ag tech startups. Another growing risk is the blurring of the lines between farm equipment dealers and agronomy providers as larger farmers demand advanced digitally enabled precision tools and services.

Two recent examples of this include CNH Industrial’s acquisition of Raven and Deere & Co.’s acquisition of Bear Flag Robotics. Both will help the original equipment manufacturers accelerate their offerings of autonomous and precision farming services, something that will compete with traditional agronomic advice provided by ag retailers.

The consolidation of U.S. farms into larger farming enterprises is a long-term structural risk for retailers

The number of U.S. farms continues to decline via consolidation as family and non-family farms seek greater economies of scale to boost profitability. While the total number of domestic farms dropped by 7.8% between 1997 and 2017, the number of large farms (defined as 2,000 or more acres) rose by 14.4% during this period.

We see these as the associated risks as this trend continues: 1) Retailers could lose their “agronomy edge” as the new class of commercial farming enterprises hire their own agronomy staff and demand more data-intensive precision ag services. 2) The larger the farm, the more likely the customer will demand volume-based discounts creating a double-edged sword for the local cooperative: selling at a discount depresses margins, but refusing to discount may force customers to purchase elsewhere.

So how should ag retailers increase their relevance to larger farm customers? More precision agronomy services

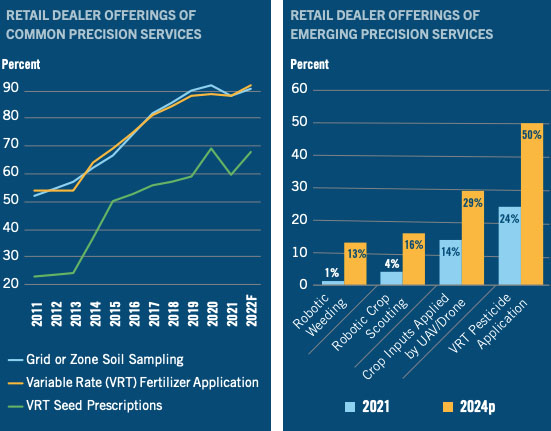

The 2021 CropLife magazine/Purdue University Precision Agriculture Dealership Survey confirmed that ag retailers continue to embrace data and digital tools (at some level) as part of their precision agriculture service offering to farm customers. While the survey indicated already strong adoption of certain sensing-technologies (such as grid or zone soil sampling) and variable rate technology (VRT) for fertilizer application, there are still tremendous growth opportunities for retailers for other technologies. Examples include unmanned aerial vehicle (UAV)/drone imagery sensing for crop scouting and analysis, VRT pesticide applications, and precision seed recommendations and prescriptions. Longterm, several new technologies offer exciting growth potential, such as crop inputs applied using UAV/drones, and robotic crop scouting and weeding.

The business case for adding software income is financially compelling

Based on our analysis of an aggregated composite of CoBank farm supply cooperatives (FSC) in two Midwestern states, FSC margins average just 2% compared to 16% for software providers. The large variance reflects lower gross profit margins for commissions on crop inputs as well as higher fixed costs for the cooperative business model. Beyond providing farm customers with enhanced digital tools to farm more profitably, the business case for retailers’ expansion of precision agronomy services is financially compelling. The higher the margin, the more patronage the cooperative can presumably pay to its membership.

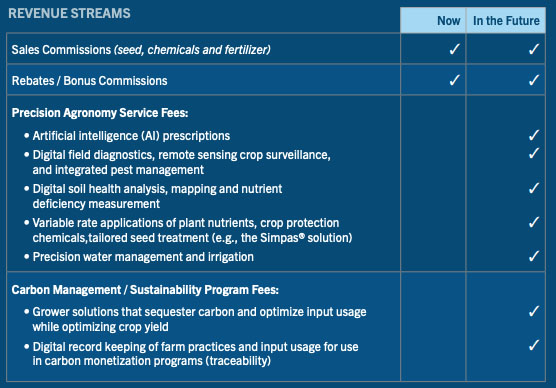

The ag retailer of the future will earn income from precision, carbon and sustainability programs in addition to traditional input product sales

The key for ag retailers is to adopt and adapt to new technology and transform the business model to generate fees for advice rather than rely on commission and rebate income from input product sales. Why should cooperatives transform? The answer is three-fold:

- Precision agronomic services are in demand by customers.

- These services can help cooperatives attract and retain high-value customers.

- If retailers do not embrace changing market needs and preferences, equipment dealers and disruptive new entrants will step up and fill the void.

Conclusion

References Farm supply cooperatives are currently experiencing cyclically strong returns as the grain run enters its second year of an upturn. Growing global demand for feed grains and vegetable oil generally positions U.S. farmers and retailers for continued success over the next year (although product shortages and high fertilizer prices could cause some disruptions). The much bigger question is what does the environment for ag retailers look like after 2023?

We see several structural risks facing farm supply cooperatives in the coming years, namely: larger, more sophisticated farm customers seeking advanced technological tools, increased competition from input suppliers and equipment dealerships providing precision agronomic services, and disruption by ag tech startup companies. However, we believe the aforementioned challenges present an opportunity for cooperatives to transform their business model to survive and thrive in the future. Putting technology and information to work to help farmers manage their inputs and production is where farm supply co-ops excel.

The path forward is to expand this delivery of precision agronomy tools, services and processes, and earn fee income for doing so. The current upturn in the crop cycle provides a timely opportunity to make the necessary investments in technology-experienced staff who can develop revenue sharing partnerships with partners across the value chain.